Four million more home mortgages nationwide would have been made between 2009 and 2013 if credit standards had been similar to 2001 levels, according to a new report from the Urban Institute.

Four million more home mortgages nationwide would have been made between 2009 and 2013 if credit standards had been similar to 2001 levels, according to a new report from the Urban Institute.

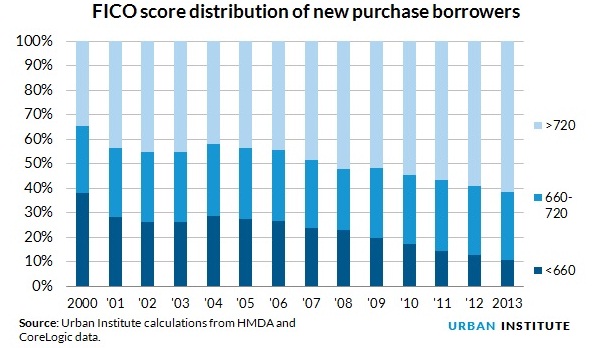

“Mortgage credit today is much tighter than it was at the peak of the housing bubble in 2005 and 2006, which is expected and appropriate. But it is also significantly tighter than it was in 2001, prior to the housing crisis. The factors contributing to the tight credit box are complex, ranging from the issue of lender overlays due to repurchase risk, to the high costs of servicing delinquent loans, to fears of litigation by the Department of Justice, the HUD Inspector General, or State Attorneys General” the report explains.

Due to the harmful impacts both on potential home buyers and the larger economiy, the report calls on policymakers to strengthen ongoing efforts to improve credit access by

- Resolving the uncertainly surrounding agency repurchases

- Evaluating why the costs of servicing delinquent loans are so high and

- Reassuring lenders that costly litigation does not lie behind every default.