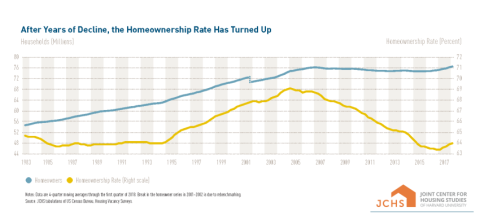

The annual report on housing from the Joint Center for Housing Studies of Harvard University (JCHS) reveals that although homeownership rates are beginning to climb, young adults are finding it increasingly difficult to afford to buy their first home. The report found that from 1990 to 2016 the median home price rose 41 percent faster than overall inflation, outpacing wage growth during the same period. Homeownership rates among young adults today are lower than they were before the recession. This report comes as VHFA and many in the lending, real estate, and housing communities recognize June as national Homeownership Month.

The past decade was marked by rapidly increasing demand for rental housing. As the economy has improved, households are now slowly beginning to reenter the homebuyer market. However, the inventory of existing single-family homes for sale across the country is currently at the lowest level since the National Association of Realtors began tracking national sales in 1982. Lower-cost homes are especially scarce. A major factor responsible for the limited inventory is the slow pace of new construction of single-family homes, which the report attributes to continued builder caution following the 2008 housing market crash, increasing construction costs, and a dwindling supply of buildable lots in metro areas where demand is highest.

Barriers to enter homeownership also put pressure on the rental housing market. The large number of households that are still struggling to enter homeownership and remain in rental housing contribute to low vacancy rates and higher rents. JCHS reports that nearly 48 percent of renters nationwide pay more than a third of their income towards housing costs, which exceeds the federal standard of affordability. When households pay more than 30 percent of their income on rent, it can be difficult to afford other basic necessities such as food, transportation, and healthcare.

Increasing income inequality is a key factor in the overall housing affordability crisis. Since the late 1980s, the median income among Americans in the key home buying age bracket of 25-34 increased only 5 percent overall when adjusted for inflation. That increase is well under the 52 percent growth in the overall United States economy (based on GDP per capita) during that time.

The report argues that programs supporting homeownership are necessary to confront a growing national affordability crisis. The ability to save enough to afford a down payment and closing costs is a significant barrier for first-time homebuyers. Affordable housing organizations like Vermont Housing Finance Agency (VHFA), which offers low down payment mortgage loans and down payment and closing cost assistance, and NeighborWorks(R) Homeownership Centers, which provide financial readiness, home buyer education, and assistance programs are critical for helping young home buyers purchase their first home.